As retirement approaches, individuals often explore investment options to secure their financial future as their salaried income decreases. In New Zealand, rental properties have long been popular due to the deductibility of interest payments and the ability to leverage capital by taking on debt. Additionally, unlike Australia or the United States, New Zealanders have not had significant incentives to participate in retirement savings schemes. This has led many people to invest in Property as a way to grow wealth. However, as people transition into retirement, the focus often shifts from wealth generation to creating a steady income stream from investments and reducing investment risk. We discuss important considerations for those holding investment properties as they enter retirement.

As retirement approaches, individuals often explore investment options to secure their financial future as their salaried income decreases. In New Zealand, rental properties have long been popular due to the deductibility of interest payments and the ability to leverage capital by taking on debt. Additionally, unlike Australia or the United States, New Zealanders have not had significant incentives to participate in retirement savings schemes. This has led many people to invest in Property as a way to grow wealth. However, as people transition into retirement, the focus often shifts from wealth generation to creating a steady income stream from investments and reducing investment risk. We discuss important considerations for those holding investment properties as they enter retirement.

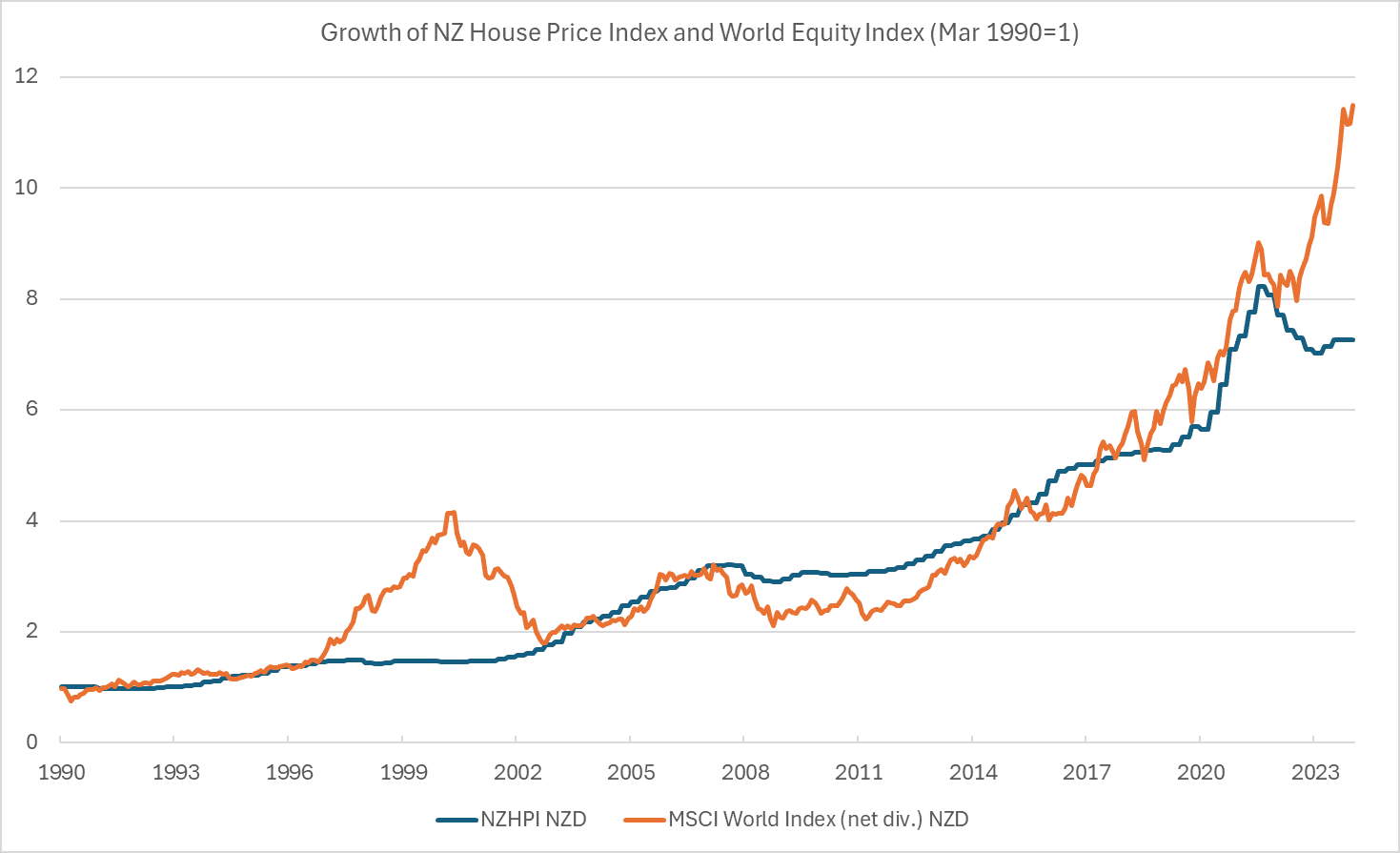

Property prices in New Zealand

Property investments in New Zealand have historically given healthy returns due to factors such as population growth, restricted supply, building cost inflation, favourable regulation, and debt-fuelled investments. The additional benefit of no capital gains tax and the deductibility of mortgage interest payments further enhance the appeal of property investments.

To illustrate this, since 1990, the New Zealand House Price Index, which is a broad measure of house price changes in New Zealand, has returned 6.2% per annum. The chart below shows the growth of one dollar since 1990 for the New Zealand House Price Index against the MSCI World Index (a common benchmark for global shares). There are periods where one outperforms the other, and we have not considered tax implications, but the comparison demonstrates that historical performance is good for both data series, highlighting that alternative properties exist.

What differs in retirement?

Reduction in investment risk appetite

As individuals move into retirement, their risk tolerance often decreases as they become more financially dependent on their investments. There are usually no salaried earnings to help with expenses, and NZ Superannuation is not enough to fully fund retirement lifestyles. The wealth that was created during working years now needs to be managed carefully to sustain retirement and to pass on to the next generation.

Income requirements increase

While rental property investment can generate steady income through tenant payments, the actual income can vary based on location, property type, market conditions,s and ownership expenses. If the rental yield is low, other investment options might offer better returns. We illustrate this in the example below, where capital of $650,000 is invested in a rental property, with tenants paying $450 per week. Once expenses and taxes are subtracted, the Property generates a net income of $12,300, or a yield of .9%. Property is managed by a company, then the cash yield reduces to .6%. As we will see later, this is relatively low compared to returns from a conservative investment portfolio.

| Self Managed | Management Company | |

| Rental Income | $23,400 | $23,400 |

| Management Fees | $0 | -$2,340 |

| Maintenance | -$2,000 | -$2,000 |

| Insurance | -$3,000 | -$3,000 |

| Rates | -$3,500 | -$3,500 |

| Gross | $14,900 | $12,560 |

| Nett (tax at 17.5%) | $12,293 | $10,362 |

| Yield | 1.9% | 1.6% |

Increased availability of capital

Rental properties are illiquid assets, meaning they cannot be quickly converted to cash. This lack of liquidity can be problematic in retirement when immediate cash might be needed for unexpected expenses or emergencies. Retirees may want to draw down capital to support their lifestyle or assist family members. However, extracting capital from a rental property often involves creating debt, which might not be desirable or feasible.

Other considerations for retired investors with rental properties

Diversification

Investment experts talk about the benefits of diversification and how this provides a smoother investment journey and reduces risk. Many property investors don’t consider the risks of investing in only one type of asset. A portfolio of investment properties that is concentrated in one asset class and one country is not diversified, increasing the risk of underperformance if that asset class does not perform as expected.

Management and maintenance

Owning rental properties requires ongoing maintenance and management, including repairs, renovations, property management fees, council rates, and insurance costs. These expenses can fluctuate, potentially reducing rental income and overall profitability. Unexpected maintenance issues can be financially burdensome, especially for retirees on fixed incomes.

Regulation and tenancy issues

Managing rental properties demands time, effort, and expertise. Self-management can be labor-intensive and may not suit retirees seeking a relaxed lifestyle. Professional property management services incur fees, impacting the Property’s return on investment.

What are the alternatives?

While direct comparisons can be challenging, we can examine a rental property alongside a conservative investment portfolio consisting of 40% shares and 60% onds. This type of portfolio should be highly diversified across global markets, providing income and growth potential. Additionally, the investments in this portfolio can be sold easily, allowing for quick access to cash through capital gains or income, making it a flexible and efficient option for generating needed liquidity.

A return of around 4.5% per annum after taxes and fees for such a portfolio is a reasonable assumption. Returning to our capital of $650,000, this would generate $29,250 per annum on average without reducing capital. A significant increase in the $12,293 from the real Property. If more cash is needed, then drawing on some capital is also an option.

The table below summarises some of the factors that we have discussed that could be considered when investing during retirement.

| RenProperty (no debt) | Real Property (with debt) | Portfolio of shares and fixed income | |

| Income Generation | Low | No | Yes |

| Capital Gains Taxed | No | No | Some |

| Historical Performance | Good | Good | Good |

| Liquidity | Low | Low | High |

| Risk of extra capital input | Yes | Yes | None |

| Diversification | Low | Low | High |

| Capital Drawdown | Hard | Hard | Easy |

| Risk of regulatory changes | High | High | Low |

Conclusion

Rental property investment can provide income and wealth accumulation in retirement, but these investments also come with challenges. While rental income offers some cash flow, investors must manage illiquidity, maintenance costs, tax implications, and management fees.

With new regulations in place looking to reduce the pace of house price growth, and with KiwiSaver becoming more common as a retirement savings vehicle, the popularity of investment properties may reduce.

Whether rental properties are suitable for retirement depends on individual circumstances, and retirees should conduct thorough due diligence, seek professional advice from financial advisers in Christchurch and tax advisors, and develop a comprehensive investment plan that aligns with their retirement objectives and lifestyle preferences.