While the last several years have seen many international share markets delivering strong double-digit investment returns, the first three months of 2026 saw most markets taking a small step backwards.

Market declines can happen at any time, but the primary headwind this quarter was linked to the escalating conflict in the Middle East. US and Israeli missile strikes on Iran disrupted the flow of oil through the Strait of Hormuz and created uncertainty for the global economy. Following the initial strikes, oil prices quickly surged from around USD 70 per barrel to above USD 100 per barrel. This eroded investor confidence in future corporate profits and led to increased risk aversion from investors, both of which contributed to lower share prices.

Market declines can happen at any time, but the primary headwind this quarter was linked to the escalating conflict in the Middle East. US and Israeli missile strikes on Iran disrupted the flow of oil through the Strait of Hormuz and created uncertainty for the global economy. Following the initial strikes, oil prices quickly surged from around USD 70 per barrel to above USD 100 per barrel. This eroded investor confidence in future corporate profits and led to increased risk aversion from investors, both of which contributed to lower share prices.

Throughout March, investor sentiment oscillated between fears of a prolonged military conflict and hopes for de-escalation.

Bond markets were similarly affected, particularly in March when most government bond prices fell (i.e. bond yields increased). The likelihood of materially higher oil prices passing through into higher inflation quickly led the market to begin pricing in

interest rate increases, even in some countries where interest rate cuts were previously anticipated.

With conflicting reports about the status of negotiations between Iran and the US, it has been difficult to guess when hostilities might ease and when markets will begin to look beyond the immediate uncertainty. However, if history is any guide, markets are adept at doing exactly that and we can expect them to eventually begin pricing in a recovery even before events in Iran can be considered anywhere near back to normal.

This concept was reinforced overnight on 8 April, with the announcement of a two-week ceasefire and a reopening of the Strait of Hormuz. Whether or not the ceasefire ultimately holds, global share markets responded immediately with a strong rebound.

Geopolitical risks elevated but not unprecedented

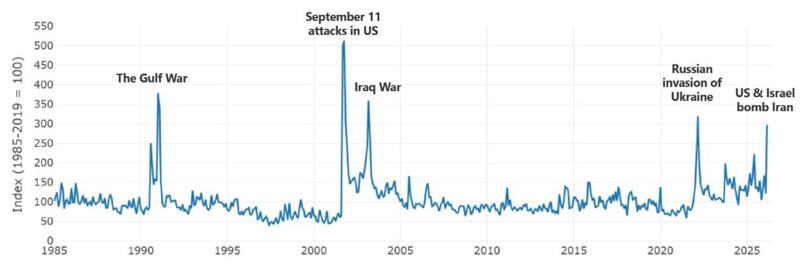

In our lifetimes, we are (at least from a New Zealand perspective) more accustomed to peace and relative geopolitical stability being the status quo. That’s why when a significant event like the recent attack on Iran occurs, it feels like the world is suddenly much more unstable.

While all major geopolitical events are uniquely different, Dario Caldara and Matteo Iacoviello (directors in the International Finance Division of the Board of Governors of the Federal Reserve in the US) developed a mechanism to enable us to compare different geopolitical risks over time. They created a Geopolitical Risk Index (GPR Index) which aggregates the occurrence of words and phrases related to geopolitical tensions that are published in leading international newspapers. This data is converted into an index number, updated monthly.

Since the mid 1980s, the GPR Index has recorded five distinct spikes, as per the following chart:

Source: Caldara, Dario and Matteo Iacoviello (2022), “Measuring Geopolitical Risk,” American Economic Review, April, 112(4), pp.1194-1225. Data downloaded from https://www.matteoiacoviello.com/gpr.htm on April 6, 2026

The index seems to do a very good job of confirming periods of escalating geopolitical instability but, as a real-time indicator, it doesn’t provide any insight into how these elevated risks might impact investment markets.

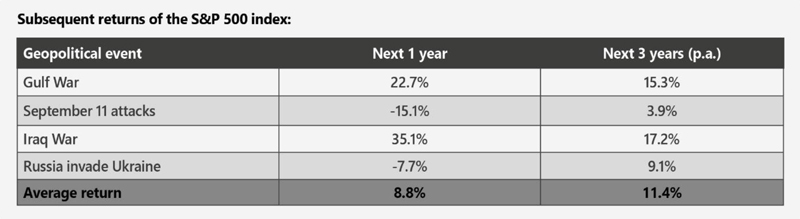

However, for that information, we can simply look back in time and calculate exactly how major markets performed from the moment those geopolitical risks first spiked. When we do this, we see the following results (based on the returns of the S&P 500 Index in the US):

Source: S&P Dow Jones Indices LLC, Consilium calculations

While we don’t have any data (yet) for the current conflict in the Middle East, the four earlier spikes on the GPR Index show average returns for the S&P 500 Index over the subsequent 12-month and three-year periods of 8.8% and 11.4% p.a. respectively. Although this is a small sample, these are, by any measure, good returns.

Without a crystal ball to tell us how the immediate future plays out, past events reveal that even when geopolitical risks are abnormally large, we can, on average, expect investment markets to continue to deliver very good long-term returns.

1970s revisited?

The recent surge in oil prices has drawn comparisons with the oil shock of the early 1970s. While there are some similarities in the geopolitical triggers and inflationary implications, the scale and market impact look to be quite different.

The 1973–74 period was characterised by a severe and sustained supply shock following the OPEC oil embargo when Arab member states stopped exporting oil to nations supporting Israel. This caused the oil price to rise from around USD 3 per barrel to over USD 11 per barrel in a matter of months, an increase of roughly 300–400%. This sharp rise fed directly into inflation, contributing to a period of stagflation across developed economies.

To use a sporting analogy, stagflation is a real coach-killer. It is an economic malaise typified by low growth, high unemployment (i.e. stagnation) and increases in consumer prices (i.e. inflation) and it’s an environment that investment markets usually detest. This was indeed the reaction in the early 1970s as the S&P 500 Index declined approximately -15% in 1973 and a further -26% in 1974, resulting in a two-year market decline of almost -40%. The combination of surging inflation, tightening monetary policy, and recessionary conditions created a deep and prolonged bear market.

In contrast, the oil price shock related to this year’s events has been much less severe. Oil prices rose from around USD 70 per barrel (pre conflict), to around USD 120 per barrel in early March, and have eased to about USD 90-100 per barrel at the time of writing (early April). In other words, we’ve witnessed a ‘peak’ price spike of around 70% and a ‘current’ price increase, while ceasefire discussions are developing, of around 35% versus early 2026 prices. Although painful, this is a far cry from the 300-400% price increase experienced in the 1970s.

The share market impact has, so far, also been much less severe. Since the commencement of hostilities on 28 February, the S&P 500 Index declined by -7.8% until 30 March. However, on that date the first suggestions of ceasefire talks began to emerge and the index rebounded by +2.9% the next day and has recovered by +7.5% to 10 April, rapidly approaching the prior share market peak.

These adjustments, in both oil prices and share market valuations, are more reflective of a cyclical shock than the prolonged structural shift experienced in the 1970s. Assuming an enduring ceasefire eventually takes hold and safe passage through the Strait of Hormuz returns, the current upheaval is very unlikely to have a protracted 1970s-style impact on economies or markets.

AI remains a key theme

Artificial intelligence (AI) remained a topical long-term investment theme over the quarter, with further evidence of its broad economic impact continuing to emerge.

In particular, the news related to AI developments was characterised by two main themes:

1. The significant ongoing capital expenditure by major technology firms into AI infrastructure

2. The expansion of AI applications into business software, healthcare and industrial processes

While AI-related shares had already delivered strong returns in prior periods, the narrative evolved during the recent quarter. Investors began to focus less on general AI hype and much more on the pathway to monetisation of the significant sums being invested in AI, and on tangible productivity gains available to underlying users of the technology.

What resulted was a more nuanced shift in the market. Rather than hype leading to the majority of AI companies rising or falling together, the quarter was notable for a more differentiated market response related to the specifics of underlying businesses.

In simple terms, companies that could demonstrate clear earnings benefits from AI were rewarded, while those with less obvious pathways to profitability saw more muted performance.

For long-term investors, AI remains a structural growth driver. The first quarter price action simply reinforced the importance of valuation discipline, as AI-related businesses, priced more on fundamentals such as profitability, tended to outperform.

Tariff update

In yet another twist in the ongoing tariff saga, on 20 February the US Supreme Court ruled that the US administration’s imposition of ‘reciprocal’ tariffs in 2025 under the International Emergency Powers Act was unlawful.

President Trump responded swiftly to this setback, imposing a 10% global tariff on all imports for up to 150 days under separate Trade Act legislation.

The Supreme Court’s ruling raised considerable uncertainty over the fate of the tariff revenue already collected, and more than 1,000 companies have now filed lawsuits in the US Court of International Trade to secure their share of the estimated USD 166 billion in illegal collections.

President Trump is scheduled to travel to Beijing in May, with the Supreme Court ruling likely to have strengthened China’s negotiating hand ahead of those talks.

New Zealand Inc

Closer to home, the Reserve Bank of New Zealand (RBNZ) left the Official Cash Rate unchanged at 2.25% on 18 February, reminding markets that the economic recovery is at an early stage and that stimulatory policy is likely to be required for some time.

It also noted that the recent increase in annual inflation to 3.1% was heavily influenced by increases in ‘administered’ prices that monetary policy has very little impact on (i.e. electricity costs, council rates etc). Outside of these, components of the non-tradables basket that are generally more sensitive to monetary policy changes were already considered to be close to average or acceptable levels.

Post the February announcement, the Iran war has led to a worsening in New Zealand’s inflation outlook and the RBNZ is currently forecasting a temporary spike in headline inflation to 4.2% in the second quarter. The largest contributor to this is higher energy and transport costs resulting from the disruption to oil supplies.

At the moment, the RBNZ’s strategy is to ‘look through’ this temporary spike in inflation, until greater certainty around the conflict in the Middle East and the potential impact on long-term oil supplies and prices is clearer.

If the positive trajectory of peace talks is maintained and oil market pressures continue to ease, the more likely scenario for New Zealand is that the economic recovery that was previously thought to be underway in the first quarter of 2026, will be delayed until later this year or early 2027.

Zoom out, not in

While certainty about the future would make our lives a lot easier, that’s not the reality of the world we live in. Six weeks ago, oil was at USD 70 per barrel. The next day the US and Israel started bombing Iran and the Strait of Hormuz closed. We didn’t get the memo ahead of time, but then again, we never do.

Now there’s a ceasefire being negotiated and what happens to oil prices will be directly related to what occurs in those talks. The uncertainty attached to all of this has seen markets move up and down in large increments. It’s unsettling on many levels, so how can investors cope in such a volatile environment?

One answer is to zoom out, not in.

When we zoom in, we tend to be hyper-focused on the current situation, the latest news and the most recent market movements. It’s a debilitating way to view your portfolio because a bad day or a bad week feels like a bad year in your head. A volatile month starts to feel like the new normal.

It isn’t. And to confirm it isn’t, all you need to do is zoom out. Don’t focus on the last day or week or month, look instead at the last year, or two or three. If you can, look at your entire long-term investment experience.

For many investors, a longer horizon will contain periods of even worse news and volatility than portfolios are facing right now. They persisted through those periods and subsequently thrived. They will survive this one too.

Being strategically invested in a well-diversified investment portfolio is the very best way to ensure that when markets do endure, and subsequently thrive, you are ideally positioned to capture the gains that will inevitably be delivered in the future.